He noted that the digital segment is experiencing a 9% EBITDA (earnings before interest, tax, depreciation, and amortization) loss.

Lakshminarayanan reaffirmed the company’s aim to achieve profitability in its digital portfolio by FY28, with expected margins of 23–25% by that time. “We are confident. FY28 is our target,” he stated, addressing concerns regarding potential delays in this timeline.

He further mentioned that margin enhancements would result from improved performance in customer interaction platforms, a revival in the Internet of Things and media sectors, along with increased contributions from AI-driven services.

“We are witnessing positive trends in infrastructure modernization spurred by artificial intelligence (AI). Our digital portfolio has seen a 15% growth,” he commented.

The company is emphasizing new product launches, expanding its AI cloud offerings, and enhancing its software-as-a-service (SaaS) solutions to propel the next growth phase. Management is set to launch three AI-focused SaaS-type products this month, which they believe could significantly improve margins if widely adopted.

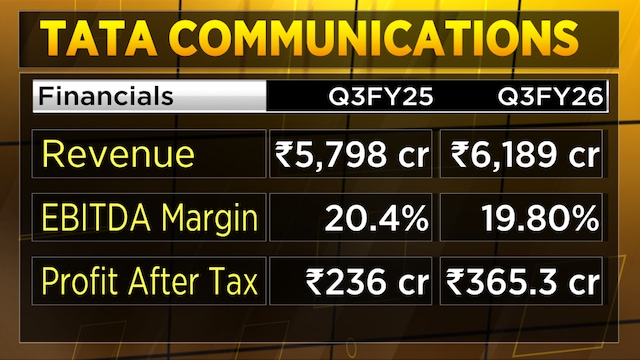

Tata Communications reported a 1.5% quarter-on-quarter increase in revenue to ₹6,189 crore for the October-December quarter of 2025 (Q3FY26), up from ₹6,100 crore. The earnings before interest, taxes, depreciation, and amortization (EBITDA) margin rose to 19.8% from 19.25%, and profit after tax jumped to ₹365.3 crore from ₹183 crore.

The company’s market capitalization totals ₹44,743.58 crore, while its shares have decreased by nearly 7% over the past year.

These are edited excerpts from the interview.

Q: Can you provide an overview of the demand outlook? Excluding FX fluctuations, topline growth was only 0.5% quarter-on-quarter and 2.2% year-on-year. Does this seem low?

A: One key point to highlight is that core connectivity makes up nearly 50% of our overall portfolio, which has historically grown at low single-digit rates. Previously around 5–6%, it has recently dipped to about 2% due to cable cuts and other impacts.

However, the digital portfolio is performing well. Considering the prevailing macro conditions, we observe positive trends in infrastructure modernization due to artificial intelligence (AI). Our digital segment has achieved 15% growth. Overall, we are pleased with the business momentum.

Q: Let’s discuss the digital portfolio, which is the main growth driver. The topline grew 15% year-on-year, but the EBITDA remains negative. Can you share the EBITDA loss for Q3 and timeline for breakeven?

A: We’re not disclosing specific numbers, but we previously mentioned a 9% EBITDA loss for the overall digital portfolio.

This portfolio consists of several major areas. The network domain and next-generation connectivity are performing well in terms of both margins and growth. Similarly, the cloud and security segments are faring well.

The other three sectors—customer interactions with Kaleyra, CPaaS, and SMS—have muted margins globally. We intend to enhance these margins by diversifying from SMS to other channels like voice and Rich Communication Services (RCS), while developing a full agentic AI through the acquisition of Commotion to improve profitability.

Also Read: Housing, retail, and SME to drive next phase of growth: Tata Capital CEO

The IoT and MOVE segments have been a drag on margins. We’re currently pivoting this business model to focus more on profitability before emphasizing growth.

The media acquisition with Switch continues to incur losses, but we anticipate reaching breakeven soon, which will support our journey toward overall digital portfolio profitability.

Q: Is there a timeline for breakeven in the digital portfolio?

A: We’ve set FY28 as our aim. Our goal is at least 23%, which is the lower end of the 23–25% margin range we provided, and we’re confident of achieving it.

Q: So, you aim for FY28 to reach your target margins of 23–25% and to break even in the digital portfolio. Am I understanding correctly?

A: Yes.

Q: Some fears have emerged that the break-even target may be pushed from FY28 to FY29.

A: That is possible; there are many variables at play. It also depends on the product mix.

This quarter, for instance, our CIS revenues grew 10% QoQ, driven mostly by CPaaS, which has lower margins. We’re also introducing several new offerings this month to accelerate enterprise digital infrastructure for AI, including three new SaaS-like products launching at the end of the month, which could help us achieve our margin goals sooner if adoption is strong.

We might even meet these targets ahead of schedule.

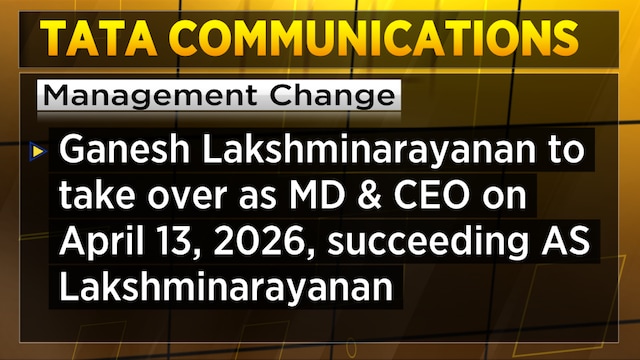

Q: I’m trying to pin you down on specifics after the announcement of a new CEO in April. Is the break-even for the digital portfolio firmly set for FY28, or is it uncertain?

A: No, we are certain. As I mentioned earlier, when you asked about 2026-27 (FY27) break-even, I specified FY28.

Q: Will we maintain the 15% topline growth in the digital portfolio, considering the order book and funnel?

A: Definitely. We expect momentum to build in the second half of 2025-26 (FY26), which we hope will continue into FY27 and FY28.

Q: What will the digital portfolio’s contribution to overall data revenues be? Currently, it’s around 50%, but as it continues to grow, what do you project?

A: We anticipate it will rise to 60% as a next goal. When we reach the ₹28,000 crore milestone, the digital portfolio will comprise slightly over 60%.

Q: Did you consider any acquisitions to reach your target of ₹28,000 crore in data revenue by FY28? There haven’t been any announcements for M&A in Q4FY26. When can we expect one?

A: We announced the acquisition of Commotion, an AI startup, this quarter. We are optimistic about this unique capability.

The voice-to-voice model they have is among the best globally, not just in India. They have adopted a comprehensive approach to AI, using an AI operating system that integrates with existing customer systems, facilitating rapid deployment of agentic AI and voice AI.

Also Read: Tata Technologies confident of double-digit topline growth in FY27

That’s one announced acquisition. Regarding further acquisitions, we are always exploring opportunities. However, acquisitions will not be pursued solely for revenue growth; they must add capabilities and strategically align with our objectives.

Q: Regarding the AI cloud economy, you previously mentioned a partnership with Nvidia and having 1,000 GPUs, but the revenue from that has been low.

Can you provide an update on the monetization of this GPU business?

A: Absolutely. We initially had 500 GPUs in partnership, and we added the remaining 500 towards the quarter’s end. Our monthly AI cloud revenue has shown promising growth, and we expect to double that this quarter and again next quarter.

Our primary focus has been on serving large enterprises. Many enterprises are still in the experimentation phase rather than on a large scale, and we are closely collaborating with them.

As part of our strategy, we are introducing our AI Studio, which will leverage this GPU-as-a-service offering. It’s launching at the end of this month with a few beta customers, representing another growth area for us.

The Commotion platform’s voice-to-voice AI model has also been trained on our Vayu AI Cloud, although it can operate on other clouds as well. This will give us a comprehensive stack of AI cloud capabilities, enhancing our monetization opportunities.

Q: How much is the monthly revenue from GPU-as-a-service currently?

A: We haven’t disclosed that yet. We will include it in our cloud and security segment, but we are seeing a doubling month-on-month, though it remains modest.

Q: Can you share the data center revenue? You provide the service and infrastructure instead of building data centers. What is its contribution?

A: We only report that under the broader cloud and security segment, which has been performing well. Cloud growth has been somewhat slow, but we relaunched Vayu Cloud after significant enhancements, and we expect it to make a more meaningful contribution shortly.

For the full interview, watch the accompanying video

Stay updated with the latest stock market news here

Live updates on Q3 results can be tracked here

Also, check out the latest expectations for Budget 2026 here