Rather than relying on a sales-based metric (enterprise value to sales), the brokerage is valuing the firm based on its operating earnings (EV-to-adjusted earnings before interest, tax, depreciation, and amortisation), which it deems more suitable at this point.

Jignanshu Gor, Director & Senior Research Analyst at Bernstein, stated that the brokerage is applying a 35x multiple for the food delivery business and a 30x multiple for the quick commerce segment.

Zomato showcased a strong performance in the October–December quarter of 2025 (Q3FY26), pushing its stock close to the ₹300 level. This came during a notable leadership change, as Deepinder Goyal transitioned from CEO to Vice Chairman, with Albinder Dhindsa assuming control of daily operations. Gor provided insights on the company’s results and prospective growth.

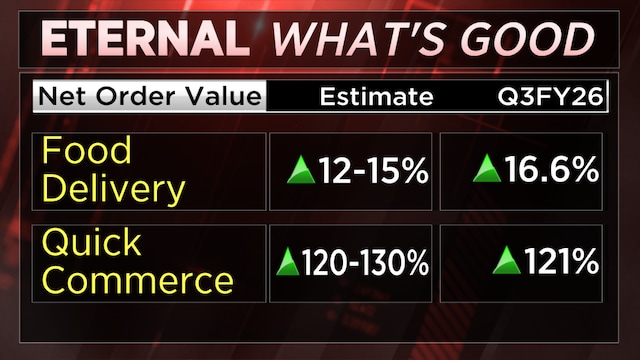

Diving into the specifics, Zomato’s quick commerce division, Blinkit, emerged as the standout performer. It achieved a growth of 121% and turned adjusted earnings before interest, tax, depreciation and amortisation (EBITDA) profitable in Q3. Gor noted this was a positive development, but added that profitability may experience fluctuations in the upcoming quarters, a sentiment echoed by the company.

Bernstein now anticipates an 80% increase in net order value (NOV) for Blinkit by FY27, with the segment attaining a positive EBITDA margin of 0.5% to 0.7% on an annual basis by that time. However, some fluctuations are expected in Q4FY26 and the following Q1FY27.

Concerning the core food delivery business, Gor mentioned it is at the “peak of its powers” both in performance and narrative. He views it as a consistent growth driver, predicting a 15–17% expansion over the next three years. He expects its adjusted EBITDA to remain stable, ranging between 5.2% and 5.5% of NOV. In Bernstein’s valuation model, the food delivery segment constitutes around 25–27% of the company’s total value.

Also Read: Bernstein points out key challenges for Swiggy and Eternal in 2026

The competitive atmosphere in the quick commerce sector is becoming fiercer. Gor confirmed that major players, including Swiggy, are aggressively vying for market share through increased discounts and lowered minimum order thresholds for free delivery. “We anticipate that growth will face challenges and may require incentivization through discounts or heightened advertising,” Gor remarked. He likened the situation to a “knife fight” which may result in “some bleeding across multiple players” over the next two quarters.

Also Read: Eternal’s quick commerce turns profitable as Goyal exits, Dhindsa steps in

On the leadership transition, Gor believes this will be a “hotly debated topic” and likely seen as a “net negative in the short to medium term.” He clarified that this perception arises because the business model is still maturing, and the stock price had benefitted from a “halo effect” tied to Deepinder Goyal’s achievements. “While a narrative pullback may occur, I believe that, given the operational results, the numbers will ultimately take precedence and the stock should perform well,” Gor concluded, maintaining a bullish outlook.

For the full interview, watch the accompanying video

Catch all the latest updates from the stock market here

Track Q3 results live here

Additionally, find the latest Budget 2026 expectations updates here