The organization is experiencing stricter safety regulations in India, which are anticipated to offer significant long-term growth visibility. Bosch Chassis Systems has shown consistent performance, achieving a revenue CAGR of 17% since FY23.

The acquisition of Bosch Chassis Systems is viewed as a strategic decision that enhances the company’s product lineup and is financially beneficial.

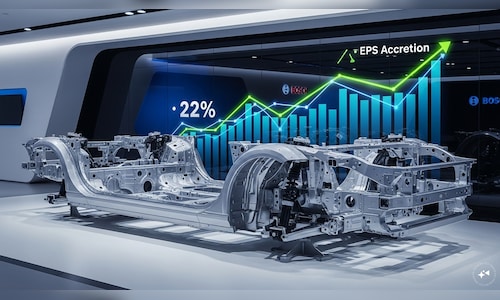

The business is highly lucrative and is projected to accelerate overall growth while enabling Bosch to assume a leading position in the future mobility landscape. The company anticipates the acquisition will increase revenue by 22% and produce an EPS accretion of approximately 5%, based on FY25 forecasts. The deal has been completed at an EV/EBITDA multiple of 10.6x for FY25.

Previously, UBS indicated that the acquisition is likely to add value from both an EPS and return ratio viewpoint, aided by minimal equity dilution and significant cash deployment.

It also mentioned that the implied FY25 EV/EBITDA multiple of 10.6x is lower than Endurance Technologies’ FY25 multiple of 21x and its one-year forward multiple of 14x.

The acquisition aims to enhance Bosch’s capabilities in safety and braking systems, while also complementing its existing power solutions division.

Bosch Chassis Systems India, representing the Vehicle Motion division of the Bosch Group in India, is a leader in automotive safety systems.

Its portfolio includes active safety technologies such as anti-lock braking systems (ABS) and electronic stability control (ESC), passive safety solutions like airbag control units and sensors, as well as braking actuation systems for passenger vehicles, two-wheelers, and commercial vehicles.